Let's be honest—if you've landed here, you're likely juggling one or more credit cards and that nagging feeling that there must be a better way to track all those balances, due dates, and eye-watering interest charges. Maybe you're asking yourself: "What's the best way to track multiple credit card debts?" Or perhaps: "How do I stop missing payments?" And here's the big one: "Should I just consolidate everything into a lower-rate personal loan and be done with it?"

You're not alone. And yes, there's a smarter way forward.

Right, let's cut to the chase. Here's your roadmap:

Here's where things get real. Credit card interest isn't just costly—it's devastatingly expensive if you let those balances linger. The Reserve Bank of Australia's indicator data shows standard credit card rates hovering around the 20% p.a. mark. Twenty percent! Meanwhile, your savings account is probably earning... what, 4%?

And the numbers are staggering. As of June 2025, Australians were carrying about 12.15 million credit cards with roughly $20.0 billion accruing interest, according to Finder's analysis. Money.com.au estimates total credit card debt sits around $42 billion. That gap? It's the difference between people who pay off their balance each month (smart cookies) and those who don't.

Which camp are you in?

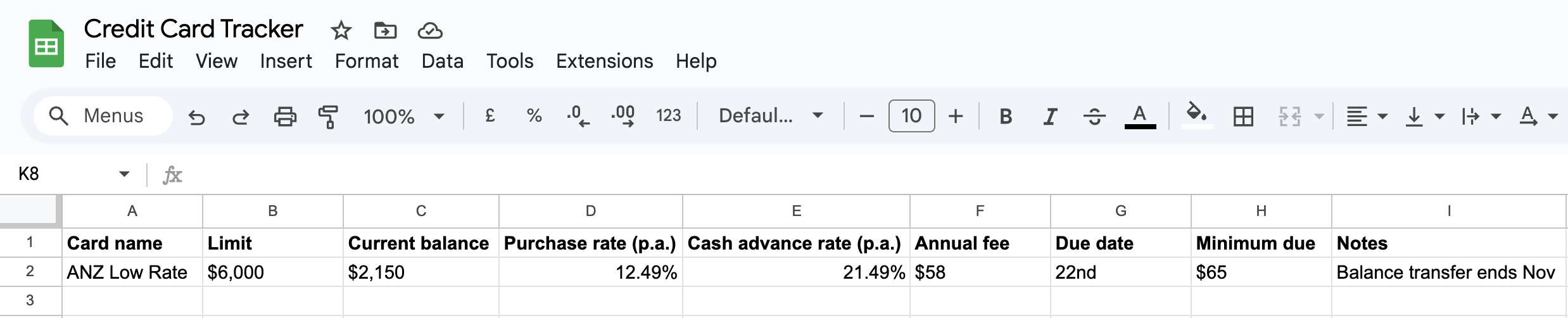

Forget fancy systems. You need something dead simple that you'll actually use. Grab a spreadsheet, your notes app, or better yet, WeMoney. If you're going old-school with a spreadsheet, here's your template:

See? Nothing fancy. But suddenly, everything's visible.

Look, you could track everything with pen and paper if you're that way inclined. But why make life harder?

This free app is basically command central for Aussie debt-fighters. Connect all your cards and watch the magic happen—every balance in one dashboard, smart alerts before bills hit, and you can even set up your avalanche or snowball strategy right in the app. Plus, it tracks your credit score (because that matters for future rates) and shows exactly where your money's bleeding out each month. Think of it as your financial reality check, served daily.

Useful for individual card notifications, sure. But they won't show you the full battlefield when you're juggling multiple issuers.

Perfect if you're a control freak who loves manual updates. Just pair it with calendar reminders, or you'll forget. Trust me.

Time to pick your strategy. And no, there's no universally "right" answer—just what works for your brain and budget.

The Avalanche Method is mathematically optimal. You attack the highest interest rate first, minimising total interest paid. It's beautiful on paper. But here's the rub: if your highest-rate card also has your biggest balance, you might feel like you're climbing Everest in thongs.

The Snowball Approach feeds your motivation. Knock out that smallest balance first, feel the rush of victory, then roll that payment into the next target. Sure, you'll pay slightly more interest overall. But if quick wins keep you in the game? Worth it.

The Consolidation Loan is the nuclear option—in a good way. Bundle everything into one personal loan at a lower rate, with a fixed end date. One payment. One date. Done.

Let's talk consolidation properly, because this could save you thousands.

Picture this: you take out one personal loan—often at a much friendlier interest rate than your cards—and use it to wipe out all those card balances. Boom. You're left with a single repayment, a fixed term, and an actual finish line you can see.

Why does this work so well in Australia right now? Credit card standard rates are stuck near 20% p.a. (thanks, RBA data), while personal loans can be meaningfully cheaper, depending on your credit profile. Plus, one repayment date means fewer late fees and a cleaner payment history—hello, better credit score.

But watch out for the traps. Check establishment fees, ongoing charges, and any early payout penalties. And whatever you do, don't stretch the loan term so far that you end up paying more total interest, even at the lower rate. That's like winning the battle but losing the war.

Let me paint you a picture with actual numbers.

Your situation: $8,400 spread across three cards, averaging 19.99% p.a. Ouch.

Option A (stay on cards): Pay $400 monthly using the avalanche method. You'll be free in about 26 months, having paid roughly $2,028 in interest. Not terrible, but not great.

Option B (consolidate): Grab a 24-month personal loan at ~11.9% p.a. Your monthly payment? About $396. Total interest? Around $1,104. You're done two months sooner and you've kept about $900 in your pocket.

That's real money. That's a holiday. Or half your emergency fund.

Ready to pull the trigger? Here's exactly how to do it right:

Ah, the eternal question. Here's the straight talk:

Balance transfers can be brilliant—0% interest for 12-24 months is hard to beat. But there's always a catch. Expect a 1-3% transfer fee upfront. And new purchases? They usually cop interest immediately unless you're paying the full balance monthly. Read. The. Fine. Print.

Consolidation loans win when you want certainty. No promotional cliff to fall off. No juggling different rates for transfers versus purchases. Just one rate, one payment, one end date. Beautiful simplicity.

Every Monday morning, while your coffee's brewing:

Ten minutes. That's it. But consistency here is everything.

Want to shave months off your timeline? Try these tricks:

Time your payments perfectly. Pay right after your salary lands—it reduces your average daily balance and therefore your interest. It's like compound interest in reverse.

Go bi-weekly. Instead of one monthly extra payment, split it into two aligned with your pay cycle. You'll reduce interest faster without feeling the pinch.

Set spending caps. Use WeMoney's category limits to stop the bleeding. That daily coffee might seem harmless until you see it's $150 a month that could attack debt.

Sweep windfalls. Tax return? Work bonus? Birthday cash from nan? Straight to debt. No negotiations.

Audit annual fees. If that premium card isn't earning its keep, downgrade or demand a waiver. Every dollar counts.

No shame here—sometimes you need help. If you're missing payments, living on cash advances, or watching minimum payments spiral beyond control, act fast.

Ring your bank's hardship team. They're actually helpful (shocking, I know). Or call the National Debt Helpline on 1800 007 007. It's free, confidential, and they've seen it all. Web chat's available too if phone calls make you anxious.

Q: What's the best app to track multiple credit cards?

A: WeMoney wins for Australians. It connects cards from multiple banks, sets smart alerts, handles avalanche or snowball strategies, and tracks your credit score. All free.

Q: Avalanche vs snowball—which is actually better?

A: Avalanche saves more money. Snowball saves more sanity. Pick based on whether you're motivated by maths or momentum.

Q: Should I close old cards after consolidating?

A: Generally, yes—it removes temptation. But if you're worried about credit score impact, keep your oldest card open with a tiny limit and no annual fee. Just don't use it.

Q: Will consolidation hurt my credit score?

A: Short-term dip from the new enquiry and account. Long-term gain from consistent payments and lower utilisation. Don't apply to multiple lenders simultaneously—that's a red flag.

Q: Balance transfer or consolidation loan?

A: Balance transfer if you can clear it within the 0% window. Consolidation loan if you want certainty or you're juggling multiple cards.

Q: How much extra should I pay?

A: Every spare dollar after essentials and a small emergency buffer. Even $50 extra monthly makes a massive difference at 20% p.a.

Q: Can I track cash advances separately?

A: Absolutely. They're usually higher rate with no grace period. List them separately and attack them first.

Three things to actually read on that statement:

"Interest-free days"—only applies if you pay the FULL balance by the due date. Carrying any balance? These don't exist for you.

"Purchase rate" vs "cash advance rate"—cash advances are the expensive emergency option. They start charging interest immediately.

"Minimum repayment warning"—this box shows exactly how screwed you'll be paying only minimums. Read it. Get angry. Pay more.

Look, the best tracking system is the one you'll actually use. And that's where WeMoney shines for Australians. Everything's in one place—every balance, every rate, every due date. The app sends alerts before bills hit (no more late fees), builds your payoff plan automatically, and shows your projected debt-free date getting closer with every payment.

Considering consolidation? Use WeMoney to verify your true balances and repayment capacity before loan

shopping. After consolidating, keep tracking to ensure those promised savings actually materialise.

Best for: Minimising total interest paid

How it works: Attack highest APR first

Watch for: Motivation lag if the highest-rate card has a huge balance

Best for: Maintaining momentum through quick wins

How it works: Smallest balance first, roll payments forward

Watch for: Slightly higher total interest than avalanche

Best for: Lower rate + simplicity + fixed end date

How it works: One loan pays all cards, you repay the loan

Watch for: Fees and extended terms that could increase total cost

Everything here is backed by real numbers. The RBA's Indicator Lending Rates (Table F5) confirm that credit card rates are materially higher than personal loan rates. Finder's August 2025 data reveals those 12.15 million cards and $20 billion in interest-accruing balances. And Money.com.au's analysis provides the broader $42 billion context.

This isn't speculation. It's maths.

Now stop reading and start tracking. Your future debt-free self will thank you.

This information is general in nature and does not take into account your objectives, financial situation or needs. It is not personal financial advice. Consider whether it is appropriate for your circumstances and seek independent advice before making financial decisions. If you're struggling, contact your bank's hardship team or the National Debt Helpline on 1800 007 007.

ABN: 88 633 007 860 WeMoney Pty Ltd

All rights reserved.

Built with ❤️ in Australia

Australian Credit Licence (ACL): 526330

WeMoney acknowledges and pays respect to the past, present, and emerging Traditional Custodians of the land in which we live and work.

.png)