If you've missed a payment, defaulted on a debt, or gone through bankruptcy, you might be wondering how long that information will follow you around. It's one of the most common questions Australians have about credit reports, and the answer isn't always straightforward.

Your credit file is essentially a financial history that lenders use to assess your reliability as a borrower. Understanding how long different types of negative information stay on your file can help you plan ahead and know when you might see your credit situation improve.

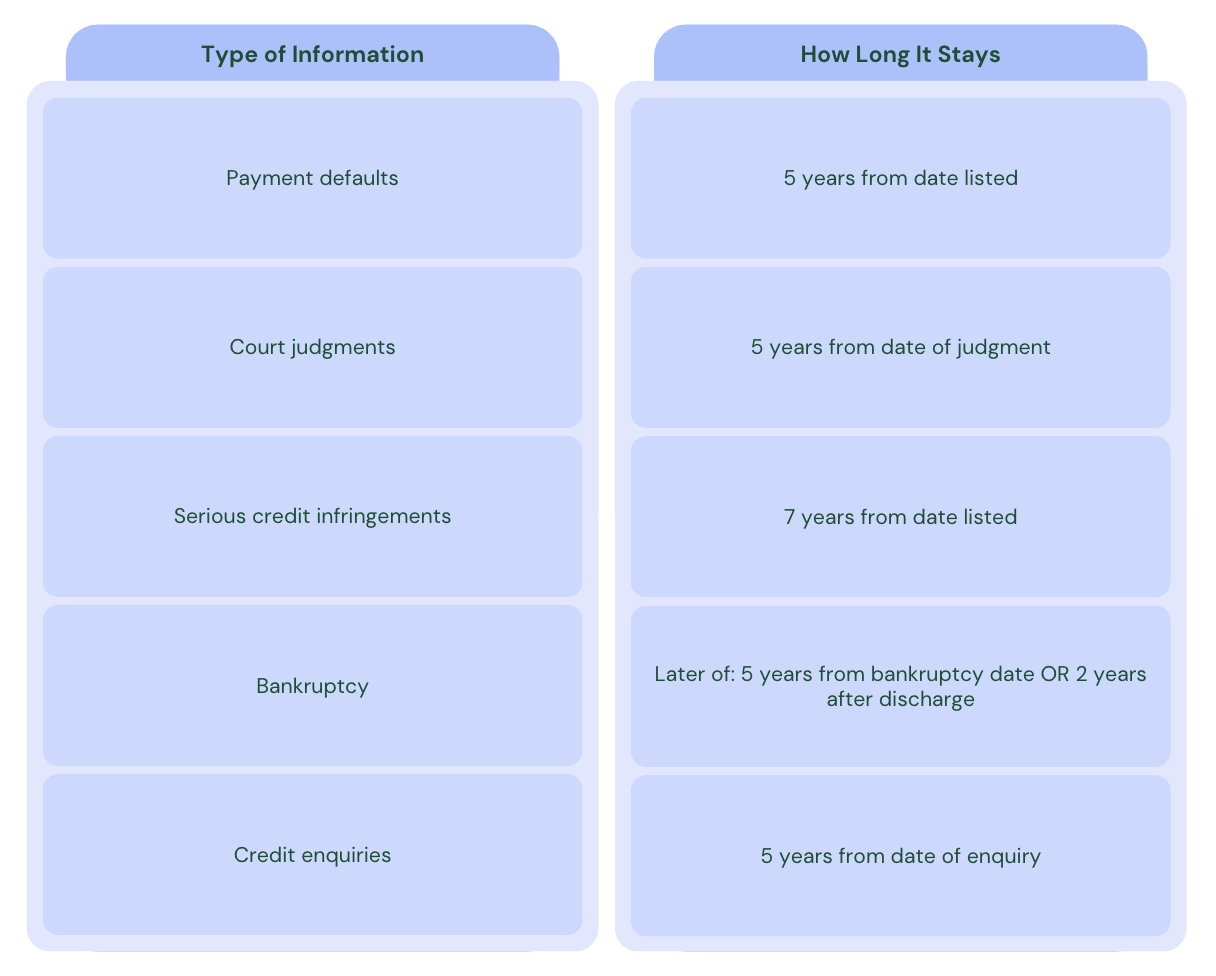

In Australia, the retention periods for negative information on your credit file are regulated by the Privacy Act 1988 (specifically Part IIIA). While many types of negative information stay on your credit file for five years, some can remain for longer periods.

According to guidance from the Office of the Australian Information Commissioner (OAIC), here are the maximum retention periods:

Furthermore, Part IX debt agreements remain on your credit file for five years from the date the agreement is accepted or the date it ends, whichever occurs earlier, while Part X personal insolvency agreements stay on your file for five years from the date the agreement begins.

The starting point for these timeframes varies depending on the type of information, which is where it gets more complex.

A payment default appears on your credit file when you've failed to pay a debt of $150 or more that's at least 60 days overdue, and the credit provider has issued you with a formal notice.

The five year period starts from the date the default was listed on your credit file, not from when you eventually pay it. This is an important distinction that surprises many people.

If you had a default listed on 1 March 2024, it will generally remain on your file until 1 March 2029, regardless of whether you pay it off in 2024, 2026, or never pay it at all. Paying the default is still important for other reasons (like stopping further collection action and showing future lenders you resolved it), but in most cases it doesn't remove it from your file any faster.

If a creditor takes you to court over an unpaid debt and gets a judgment against you, that judgment typically stays on your credit file for five years from the date it was entered by the court.

Again, paying the judgment generally doesn't remove it early, though it will show as "satisfied" on your report, which looks better to potential lenders than an unpaid judgment.

Serious credit infringements, such as providing false or misleading information on a credit application, stay on your credit file for up to seven years from the date they're listed. This is longer than most other types of negative information due to the severity of the conduct.

Bankruptcy is treated more seriously and can stay on your credit file longer than other types of negative information.

According to OAIC guidance, bankruptcy remains on your credit file for whichever is later:

For most people, bankruptcy lasts three years and one day from the date of declaration. This means the bankruptcy notation typically stays on your credit file for five years total from when you first became bankrupt (since five years from declaration is later than two years after a three year bankruptcy ends).

If you've been bankrupt multiple times, each bankruptcy is listed separately with its own timeline.

These formal debt arrangements with creditors also appear on your credit file, but the starting point varies:

Part IX debt agreement: Five years from the date the agreement is accepted or the date it ends, whichever is earlier.

Part X personal insolvency agreement: Five years from the date the agreement starts.

Both will generally show on your file even after you've completed the agreement and paid everything off, until the applicable timeframe expires.

Not all information on your credit file is negative, but it's worth knowing how long credit enquiries last since they can impact your credit score.

When you apply for credit and a lender checks your report, that enquiry stays on your file for five years. However, credit enquiries typically have a much smaller impact on your score than defaults or bankruptcy, and their influence generally decreases significantly after the first 12 months.

There are limited exceptions where information might come off sooner:

Defaults listed in error: If you can demonstrate that a default was listed incorrectly (for example, you never received proper notification as required by law, or the debt amount or dates are wrong), you may be able to have it removed through the dispute process. However, this requires proving the listing was genuinely incorrect, not simply that you've now paid it.

This is a narrow exception and doesn't apply to defaults that were correctly listed but you simply wish weren't there.

Clearout period: Some older types of negative information that were listed under previous credit reporting rules may have different removal timeframes, but this mainly affects records from many years ago.

The only way to know exactly what negative information is on your credit file and when it's due to be removed is to check your report directly.

In Australia, you're entitled to access your credit report for free from each of the credit reporting bodies (Equifax andExperian) once every three months. Many Australians check their report through services that provide ongoing access, making it easier to monitor what's there.

When you're looking at your credit file, each listing should show the date it was recorded. You can count forward the applicable number of years from that date to know when it will be automatically removed.

For more detailed information about credit reporting timeframes, you can refer to the Office of the Australian Information Commissioner's guidance.

When negative information reaches its removal date, the credit reporting body automatically deletes it from your file. You don't need to do anything or request removal; it happens as a matter of course.

Once removed, that information no longer affects your credit score or appears to lenders who check your file. Your score will typically improve when negative marks drop off, though the improvement depends on what else is on your report.

"Paying off a default removes it immediately"

This generally isn't true. Paying a default is important and will show on your file as "paid," but in most cases the listing itself stays for the full five years from when it was first recorded.

"I can pay to have defaults removed"

Legitimate credit repair doesn't work this way. No one can legally remove accurate information from your credit file before its scheduled removal date. If someone claims they can remove accurate negative information early, they're either planning to dispute the listing (which only works if it's genuinely incorrect) or they're not operating legitimately.

"Closing my credit cards removes enquiries"

Closing credit accounts doesn't remove the history of those accounts or any enquiries made when you opened them. The information generally stays for its full term regardless of whether the account is still active.

Understanding these timeframes can help you make realistic plans for future credit applications.

If you know a default will drop off your file in six months, you might consider waiting before applying for a home loan, as this could improve your chances of approval and potentially lead to better interest rates.

If you've been through bankruptcy and know it will remain on your file for another two years, you can plan accordingly and focus on building positive financial habits in the meantime.

While negative information sits on your file, you can still take steps to improve your overall credit position:

Making all current payments on time demonstrates recent responsible behaviour, which lenders value. Even with old negative marks on your file, a consistent pattern of on time payments over the past 12 to 24 months can show you've changed your financial habits.

Keeping credit applications to a minimum reduces new enquiries on your file. Consider only applying for credit you genuinely need and are likely to be approved for.

Maintaining stability in your employment and living situation, while not directly shown on your credit file, can help lenders see you as lower risk when they assess your application alongside your credit report.

Credit reporting bodies are generally reliable about removing information at the correct time, but errors can occur. If you notice that a default, judgment, or other negative listing is still showing after its scheduled removal date, you can contact the credit reporting body directly to have it investigated and removed.

You'll usually need to provide details about the listing (the date it was recorded, the creditor, and the amount) and evidence that it should have been removed, though the removal date calculation should be straightforward from the information already on your file.

While it's natural to focus on when negative information will disappear from your credit file, it's worth remembering that your credit report is just one factor lenders consider. Your current income, employment stability, savings, and overall financial situation all play significant roles in credit decisions.

Understanding your credit timeline gives you realistic expectations and helps with planning, but building strong financial habits now matters more than counting down to removal dates.

Knowing where you stand with your credit file, tracking your progress as negative marks age off, and maintaining good financial habits in the present gives you the clearest path forward, regardless of what's in your past.

This article contains general information only and is not financial advice. Everyone's situation is different, so consider seeking independent advice if you're unsure about your credit situation. For authoritative information about credit reporting timelines, refer to the Office of the Australian Information Commissioner's guidance.

Understanding your complete financial picture includes knowing what's on your credit file. WeMoney provides free access to your credit score and helps you track your financial health in one place. Monitor your credit score changes, see your spending patterns, and stay on top of your financial commitments. Download WeMoney free for iOS and Android.

ABN: 88 633 007 860 WeMoney Pty Ltd

All rights reserved.

Built with ❤️ in Australia

Australian Credit Licence (ACL): 526330

WeMoney acknowledges and pays respect to the past, present, and emerging Traditional Custodians of the land in which we live and work.

.png)