.png)

.svg)

The social financial wellness app that

helps you track and crush debt—for free.

Downloaded by over 500,000 Australians

.png)

WeMoney changes lives everyday. Check out these members’ stories and see the results firsthand.

Joined 2021

Joined 2021

Joined 2020

Joined 2021

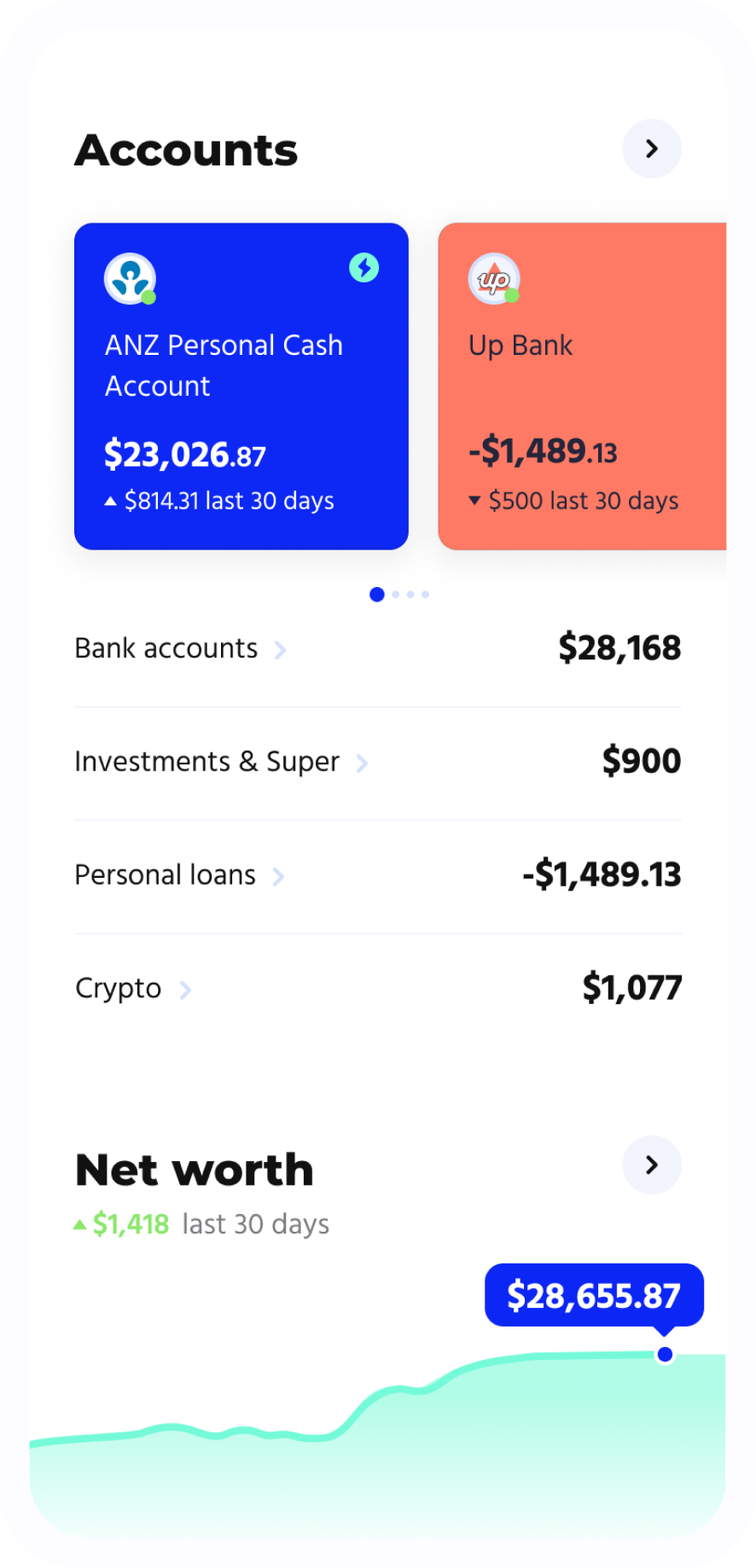

Get an overview of your money by connecting all your accounts. The magic of WeMoney tells you where you can save.

WeMoney keeps an eye on your debts and finds you personalised deals. The best part? It takes seconds to apply and be approved.

Uncover those sneaky subscriptions you forgot you were paying for.

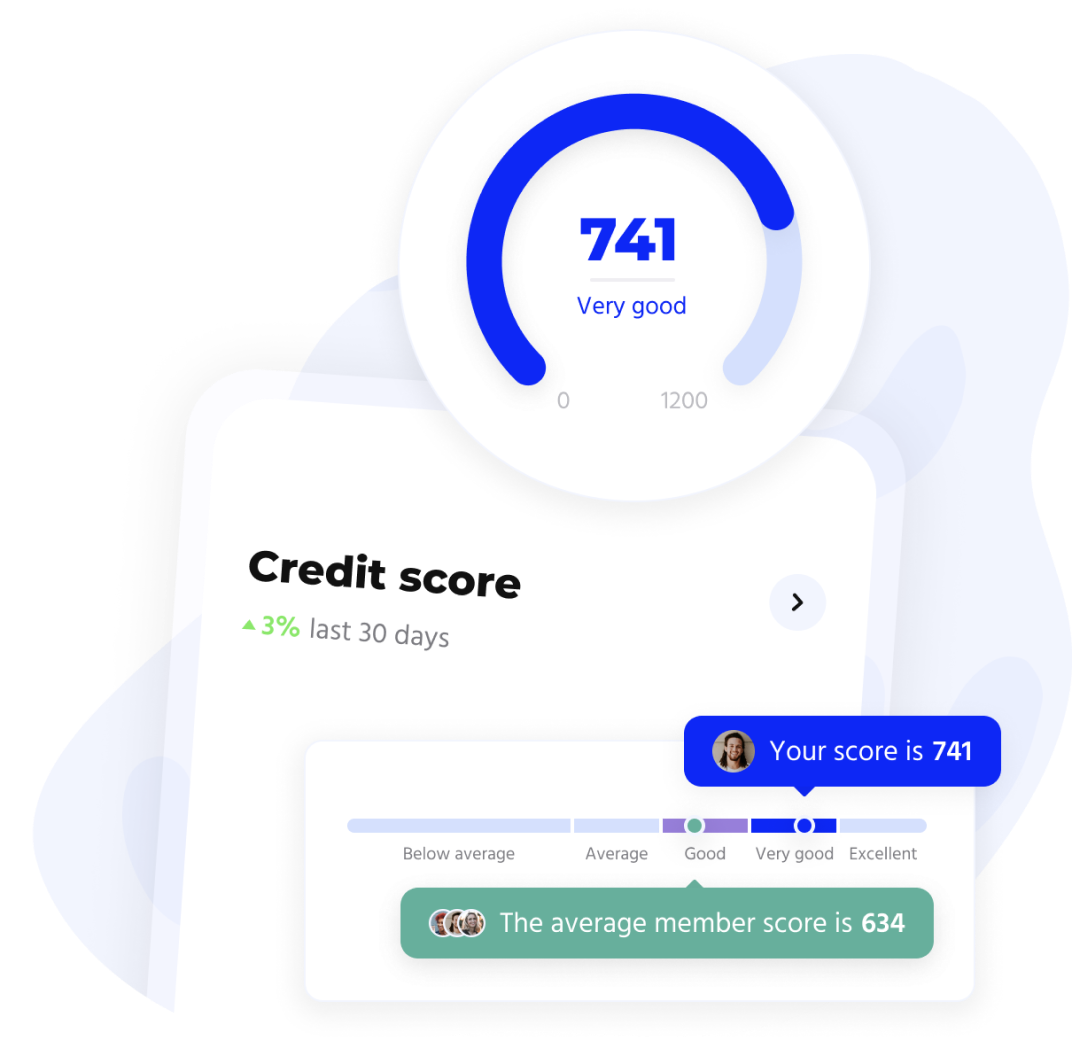

The average WeMoney member improves their credit score by 63 points just 9 months after joining.

We use the same industry-standard security practices as the leading banks. Our services are routinely inspected, tested and audited by qualified security and data specialists.

2048bit SSL encryption end-to-end whenever you use any of WeMoney services.

WeMoney partners with Yodlee, a global leader in banking technology to store your information securely. Yodlee is trusted by over 27 million users worldwide.

We never store your bank login details on our servers.

Our members are taking big steps towards healthier financial lives. See what they have to say about their WeMoney journey.

I was spending way too much in interest on a loan just to get by and found it quite stressful.

I refinanced my personal loan thanks to WeMoney, lowering my interest rate by 7%, which is huge!!

Harrington Park, NSW

.png)

The WeMoney Community gave me the hope and courage I needed to finally reach out for help.

After nearly three years of my downhill financial struggle I finally made an appointment for financial counselling.

Naracoorte, SA

I previously got into bad money habits with an ex-partner. I had built up credit card debt and a small personal loan.

WeMoney helped me consolidate my debts, saving me thousands in interest. I can now feel more confident about getting my finances on track and saving up for my first home.

Berri, SA

.png)

My dopamine now comes from watching my financial situation improve and being able to provide my son his needs—made even better with the WeMoney app!

Perth, WA

After downloading WeMoney I realised that I was dropping $60-$400 on gambling regularly with no return.

Now having this beautiful app I can track my expenses and break the cycle.

Narabeen, NSW

With COVID-19 mandates cutting our household income in half, my husband and I struggled with our credit card payments.

WeMoney really helped us, as we were able to get a new loan and pay our credit card, allowing us to save for our new goals.

Menzies, QLD

.png)

I was spending way too much in interest on a loan just to get by and found it quite stressful.

I refinanced my personal loan thanks to WeMoney, lowering my interest rate by 7%, which is huge!!

Harrington Park, NSW

I previously got into bad money habits with an ex-partner. I had built up credit card debt and a small personal loan.

WeMoney helped me consolidate my debts, saving me thousands in interest. I can now feel more confident about getting my finances on track and saving up for my first home.

Berri, SA

After downloading WeMoney I realised that I was dropping $60-$400 on gambling regularly with no return.

Now having this beautiful app I can track my expenses and break the cycle.

Narabeen, NSW

After downloading WeMoney I realised that I was dropping $60-$400 on gambling regularly with no return.

Now having this beautiful app I can track my expenses and break the cycle.

Narabeen, NSW

My dopamine now comes from watching my financial situation improve and being able to provide my son his needs—made even better with the WeMoney app!

Perth, WA

With COVID-19 mandates cutting our household income in half, my husband and I struggled with our credit card payments.

WeMoney really helped us, as we were able to get a new loan and pay our credit card, allowing us to save for our new goals.

Menzies, QLD

Subscribe to WeMoney Pro and get access to advanced features, including

Unlimited custom categories

Desktop accounts & transactions

Equifiax credit alerts

Automatic goal tracking

Turn off ads

And much more!

Learn the best tips in the industry from our finance experts.

Join Dan and special guests as they explore everything from getting out of debt to buying your first home.

Member goals set

of members have improved their financial lives since joining

Downloads

Trees planted through One Tree Planted

ABN: 88 633 007 860 WeMoney Pty Ltd

All rights reserved.

Built with ❤️ in Australia

Australian Credit Licence (ACL): 526330

WeMoney acknowledges and pays respect to the past, present, and emerging Traditional Custodians of the land in which we live and work.

.png)